There may be a completely different story behind the numbers.

According to data compiled by Redfin Corp. from 25 of the largest metro areas, the median down payment for the least expensive 25 percent of properties sold in 2013 was about $3,400 more than in 2007. And, down payments rose fastest for lower priced homes.

Interest rates remain incredibility low, but it seems to be more difficult to become a homebuyer. Challenges such as increased fees for FHA loans, higher down payments for conventional loans, tighter credit and less supply are certainly contributing factors.

But, is there more at play here?

A big part of the problem is that many first-time homebuyers, who would be looking at starter homes with lower prices, have self selected themselves out of the home buying process. They fear high down payments, not getting approved and bidding wars. loanDepot’s consumer survey found that the fear of rejection drove almost half of today’s potential homebuyers from the housing market.

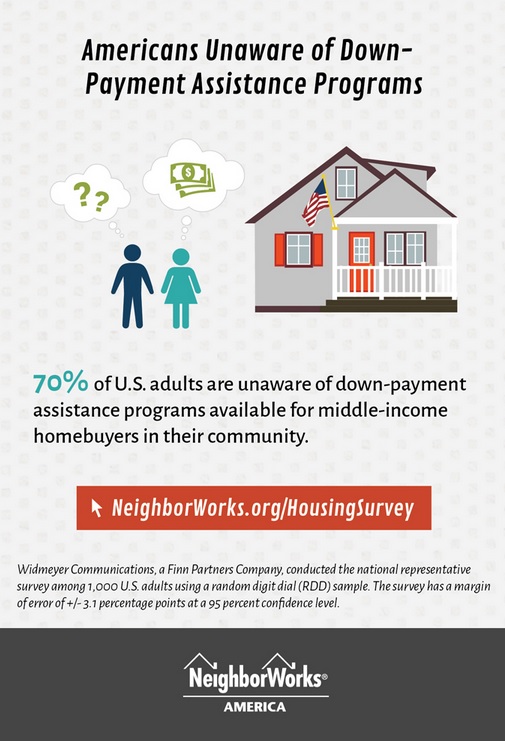

In fact, there are low down payment options and even homeownership programs that can help fund down payment and closing costs. However, those living with their parents or recommitting to a more expensive rental agreement don’t know affordable options are available through homebuyer programs and housing finance agencies.

Housing Wire reported that Nomura analysts said:

“It’s not that Millennials and other potential homebuyers aren’t qualified in terms of their credit scores or in how much they have saved for their down payment. It’s that they think they’re not qualified or that they don’t have a big enough down payment.”

To support that view, Freddie Mac recently shared a survey by Zelman & Associates that found borrowers greatly overestimate the down payment requirement. Amazingly, 60-72 percent of renters believe they need 11-15 percent to buy.

So, are down payments really rising? Yes and no. Many consumers may actually put down more for their down payment because they think it’s required. However, that doesn’t mean there aren’t low down payment and affordable home finance options available. Quite simply, renters just aren’t evaluating their options.

Now may be the best time to start the process: Zillow’s new data shows that renters are paying 29.5 percent of income in rent while homebuyers are paying 15.3 percent of income for their mortgage.